Got $10? Consider a monthly donation.

by Greta Bush

Do you ever look at your credit card bill and wonder how it got to be so high? You didn’t make any major purchases. Then you look closely…$10 spent on a whim here, $6 spent there…it adds up! I, for one, can’t be trusted to walk into Target without a strict list or my husband holding onto my hand. (I kid! Sort of…) Everything is so pretty…so innovative…so alluring. And priced at that sweet spot! Meanwhile, I get to the checkout and immediately regret my life choices.

Think about how easily you spend $10 a month on consumer products without even realizing it. Now, consider making an intentional choice to make a recurring donation of $10 a month to Habitat! Asheville Area Habitat for Humanity builds affordable, energy-efficient homes and sells them to qualified buyers at no-profit. A monthly donation to Habitat’s #build828 sustained giving club will help Habitat raise money for this cause.

We’re all guilty of blowing cash from time to time. Here are some examples of how easily that money slips from our wallets…but would be put to better use supporting Asheville Habitat:

-

Target

Let’s get real. Who only spends $10 on a Target run? Help build a house rather than filling yours with stuff from the Dollar Spot.

-

Starbucks

$10 = 2 venti caramel macchiatos. Coffee tastes sweeter made in your own home—donate your money to Habitat to help keep housing affordable!

-

Netflix

$10 is the cost of a monthly subscription. Rather than watching a family on reality TV, help change a real family’s future with a monthly donation to Habitat for Humanity.

Speaking of Netflix…

-

T-mobile

Your Netflix subscription is included if you have T-mobile…so you’ve got an EXTRA $10 a month! Why not donate that money to a good cause?

-

Spotify

$10 is the cost of a monthly subscription. Create a new soundtrack filled with the sound of kids playing safely outside in their Habitat neighborhood.

If this is ringing even a little bit true for you, click the button. Set it and forget it. #build828 is the kind of recurring spending we can all get behind!

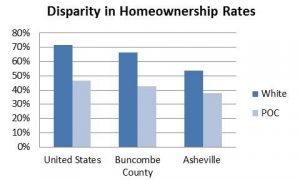

Habitat creates a way for households facing economic barriers to achieve homeownership and begin to close the wealth gap, but we can’t do it alone. To achieve equity in rates of homeownership nearly 3,000 additional households of color in Buncombe County will need the opportunity to become homeowners. To achieve this scale, we will need many more lenders to adopt policies that help households of color overcome historical barriers to mortgage loans. We need to grow housing and financial counseling opportunities to help aspiring homebuyers become “mortgage ready”. We need more affordable rental options and tenant advocacy so that renters have the stability needed to save and prepare for future ownership. Finally, we need home repair and foreclosure prevention assistance to help existing homeowners to remain at home. In short, it will take everyone committing to give our time, our financial support, and our voices to advance the dream of equality of opportunity for all our neighbors regardless of race.

Habitat creates a way for households facing economic barriers to achieve homeownership and begin to close the wealth gap, but we can’t do it alone. To achieve equity in rates of homeownership nearly 3,000 additional households of color in Buncombe County will need the opportunity to become homeowners. To achieve this scale, we will need many more lenders to adopt policies that help households of color overcome historical barriers to mortgage loans. We need to grow housing and financial counseling opportunities to help aspiring homebuyers become “mortgage ready”. We need more affordable rental options and tenant advocacy so that renters have the stability needed to save and prepare for future ownership. Finally, we need home repair and foreclosure prevention assistance to help existing homeowners to remain at home. In short, it will take everyone committing to give our time, our financial support, and our voices to advance the dream of equality of opportunity for all our neighbors regardless of race.